As you’re navigating the path to retirement, you very likely have a parade of questions marching through your mind. “What is full retirement age?” “How much will I actually pocket?” “Will Social Security truly sustain me during retirement?” Let’s roll up our sleeves and dig into some of these most pressing questions.

First, it’s important to note that Social Security was never meant to cover 100% of retirement income needs for individuals or families. On average, Social Security represents about 40% of overall income for low and median households in retirement, and about 20% for high income retirees.

To achieve a well-rounded retirement income strategy, it is imperative to coordinate Social Security benefits with distributions from IRAs, 401(k)s, savings, pensions, and other income sources to effectively meet monthly financial needs. It is important to note Social Security provides guaranteed, steady, and lifetime payments which are Cost of Living Adjusted (COLA) each year based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This inflation index closely represents the true cost of inflation, and typically exceed the inflation adjustments one can obtain with a commercially purchased annuity product.

So, how much can you expect to receive? When determining your Social Security benefit, the calculation hinges on two key factors: your earnings throughout your working career and the age at which you decide to apply for benefits. Eligibility for Social Security benefits requires a minimum of 10 years of contributions to the system, with individuals earning four credits each year by meeting a specified minimum income threshold. In total, 40 credits are needed (there are exceptions to the 40-credit hour requirement for workers needing Social Security Disability benefits).

At the age of 62, your highest 35 years of earnings, adjusted annually for wage inflation, are averaged to compute your Average Indexed Monthly Earnings (AIME). It’s important to recognize that the intricacies of this calculation play a significant role in shaping the Social Security benefits you can anticipate.

AIME is divided by three “bend points” to determine your Primary Insurance Amount (PIA) – the amount you’ll receive at full retirement age. One can think of their PIA as their ‘baseline’ benefit:

- 90% of the first $1,115 of his/her AIME +

- 32% of his/her AIME over $1,115 and through $6,721 +

- 15% of his/her AIME over $6,721

Here is an example for an individual whose AIME is $10,000

- 90% x $1,115 = $1,003.50 +

- 32% x ($6,721 – $1,115) = $1,793.92 +

- 15% x ($10,000 – $6,721) = $327.90

- Monthly PIA*: $3,125.30 ($1,003.50 + $1,793.92 + 327.90)

There are also some cases where your benefit may be reduced:

- If you worked in a job that did not pay into the Social Security system and receive a pension from that job, you may not receive your full benefit; and,

- If a spouse is eligible for a pension under a non-Social Security covered job, the spousal benefit may be reduced under the Government Pension Offset (GPO).

Now that you understand how AIME is calculated, you are likely wondering when and how you should apply for Social Security benefits. You are eligible for your individual benefit between ages 62 and 70. While there is no set guidance on when to apply, there are many factors to consider, including:

- Do I (we) need income immediately?

- Am I coordinating claiming with a spouse?

- Are there other sources of income I can rely on while I delay claiming?

- Does my health situation warrant claiming early?

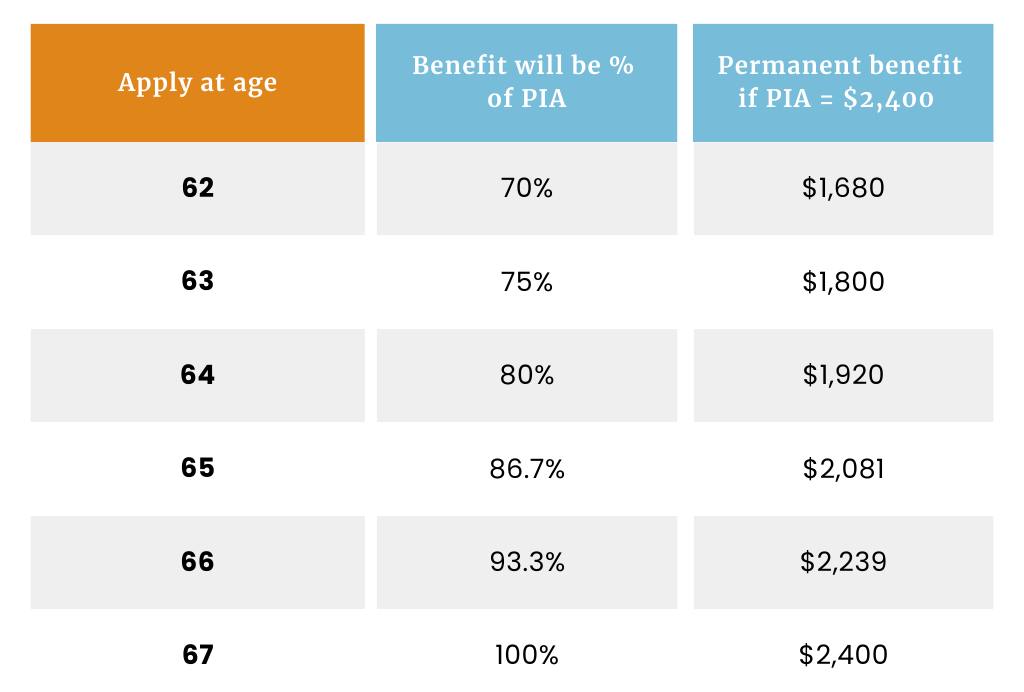

If you claim prior to Full Retirement Age (FRA), there is a permanent reduction in your benefit, called the actuarial reduction. The chart below outlines the reduction for an individual whose FRA is age 67 and whose PIA (baseline) is $2,400:

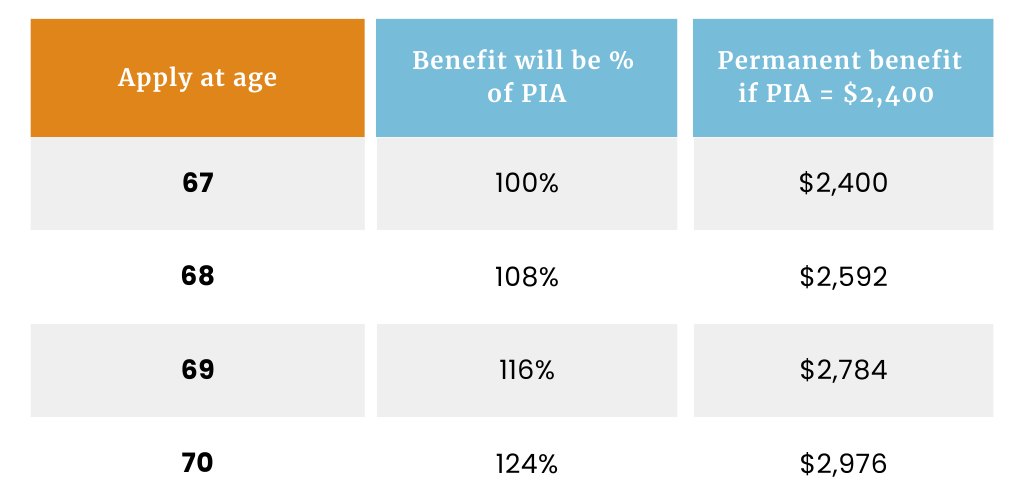

Conversely, claiming your individual benefit after FRA would result in an 8% per year increase in your benefit via delayed retirement credits. The chart below outlines the increase in one’s benefit who delays claiming past FRA for an individual whose FRA is age 67 and whose PIA is $2,400:

- Online at ssa.gov/apply

- By phone at 800-772-1213

- In person at local Social Security Office; ssa.gov/locator. Note: Survivor benefits must be applied for in person

The decision on when to claim is personal and unique for everyone. Claiming one’s individual benefit too early, or not being aware of spousal coordination rules, divorce or survivor benefits you may be entitled, may result in in potentially reduced benefits for life.

Given the complexities of Social Security claiming strategies, we recommend meeting with an advisor who specializes in Social Security strategies to review your options and help determine the optimal claiming age and strategies for you.